/ disclaimer

/ disclaimer

The relevant information in this article comes from publicly available information. This platform does not make any guarantees for the correctness, fairness and completeness of the relevant information; the content of this article only represents the judgment of the researcher at the time of publishing the article. Any changes will occur without further notice; the content of this article does not represent the recommendation of our company, nor does it constitute investment advice for investors. Investors invest accordingly and at their own risk; the copyright of this article belongs to our company. If a third party quotes or reprints, the source must be indicated, and no deletion or modification contrary to the original intention of this article is allowed.

01

market review

The futures aluminum price fluctuated and went down, and macro factors dominated the price down. The economic growth target in the government work report of the two sessions was lower than expected, which dampened market optimism. The domestic inflation data in February was lower than expected, the market lowered the domestic economic recovery efforts, the inversion of long-term and short-term interest rates in the United States intensified, and the thunderstorm of Silicon Valley Bank triggered a rise in risk aversion in the capital market, dragging down aluminum futures prices. Relatively speaking, the influence of the fundamentals on prices is relatively weak. Although consumption has maintained a recovery momentum, its performance has been relatively moderate. This makes it difficult to destock, and the contradiction between supply and demand is not prominent even if the output is lower than expected. Affected by negative macro conditions and weak demand this week, aluminum prices are under pressure.

【Futures market】

Shanghai Aluminum main contract 2303 has fallen by 2.72% this week. The initial price of this cycle is 18775 yuan/ton, the end price is 18265 yuan/ton, the highest price is 18785 yuan/ton, and the lowest price is 18215 yuan/ton.

【Spot market】

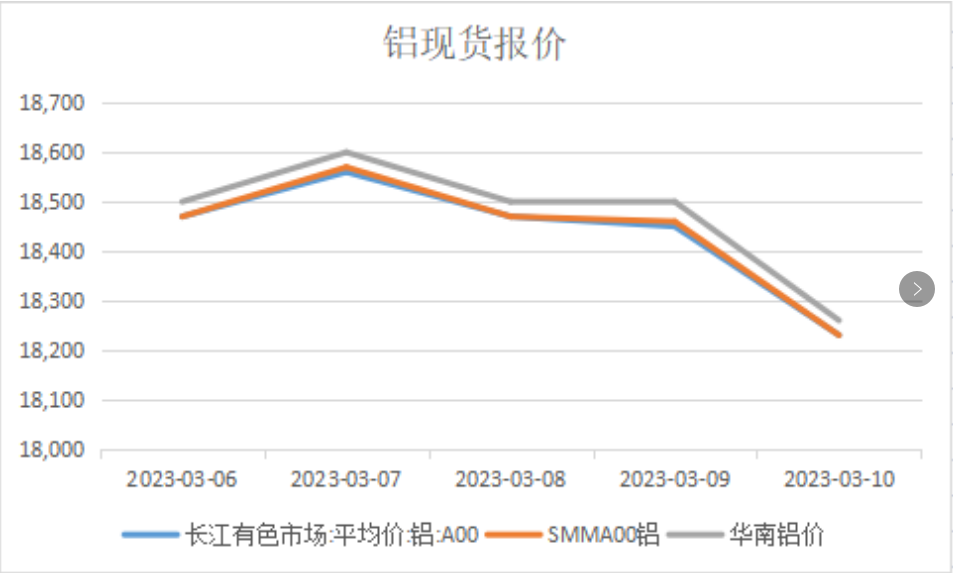

The overall performance of the spot market this week is not good. Due to the limited increase in new orders of downstream aluminum processing enterprises, although production reduction has an impact on output, the spot supply is abundant and the enthusiasm for receiving goods is not high. They mainly purchase on demand. And the trading activity among traders is not enough. However, with the price drop, the transaction has improved, because the consumption expectation in the peak season still exists. The mainstream transaction price in the East China market was around 18,500 yuan/ton, and fell to 18,200 yuan/ton on Friday. The mainstream transaction price in the South China market is in the range of 18,500-18,600 yuan/ton, and fell to 18,250 yuan/ton on Friday.

02

Premiums, Discounts and Spreads

The impact of production cuts on supply is becoming apparent, but inventories are still at a high level, and the status of spot discounts has not changed. This week's spot discount is around 60 yuan/ton, which is slightly narrower than last week.

03

Macro information this week

1. The main expected goals for China's development in 2023 are clear! According to the government work report, the main expected development goals for 2023 are: GDP growth of about 5%; new urban jobs of about 12 million; surveyed urban unemployment rate of about 5.5%; consumer price growth of about 3%; Basically keep pace with economic growth; promote the stability and quality of imports and exports, and basically balance the balance of payments; maintain grain output at more than 1.3 trillion catties; continue to decline in energy consumption per unit of GDP and emissions of major pollutants, and focus on controlling fossil energy consumption , The quality of the ecological environment has been steadily improved.

2. China's official manufacturing PMI in February was 52.6, a new high since April 2012; Caixin manufacturing PMI was 51.6, and business confidence rose to a 23-month high.

3. China's official manufacturing PMI in February was 52.6, a new high since April 2012; Caixin manufacturing PMI was 51.6, and business confidence rose to a 23-month high.

4. European Central Bank Governing Council Villeroy said that inflation is expected to peak in June this year, bringing inflation back to 2% by the end of 2024 or early 2025.

04

Fundamentals

1. Import profits

As of March 2, 2023, the closing price of LME aluminum is 2,395.5 US dollars / ton; the closing price of the main aluminum contract in Shanghai is 18,650 yuan / ton, and the import price is 1,025.58 yuan / ton. The import inversion increased by 389 yuan/ton compared with last week.

As of March 9, 2023, the closing price of LME aluminum is 2,320 US dollars / ton; the closing price of the main aluminum contract in Shanghai is 18,495 yuan / ton, and the import inversion is 718.43 yuan / ton, which is nearly 300 yuan less than last week /Ton

2. Cost and profit per ton of aluminum

The impact of the coal mine accident in Inner Mongolia on coal prices came to an end temporarily, and coal prices rebounded in a short period of time and then fell back again. Last week, the cost of electrolytic aluminum across the country fell further, mainly due to the drop in the price of prebaked anodes, and the further drop in the price of alumina in some areas, and the temporary stabilization of electricity prices. Overall, the average profit of aluminum plants has risen to more than 1,000 yuan, but because the production restriction in Yunnan is based on objective reasons, high profits cannot stimulate the release of more production. This week, with the sharp drop in aluminum prices, the profits of aluminum factories fell below 1,000.

3. Downstream start-up picks up slightly

In the week of March 3, the operating rate of aluminum profiles was 60%, +2 percentage points week-on-week; the operating rate of aluminum strips was 78.2%, +0.4 percentage points week-on-week; the operating rate of aluminum foil was 81.1%, which was flat week-on-week; the operating rate of aluminum materials was 63% %, week-to-week ratio of +1.2 percentage points. After the festival, the downstream construction gradually resumed, but the current real estate sales transactions still have no obvious improvement. Developers are still in short supply of funds, and it is difficult to pay back, which will restrict the subsequent start of construction. The inventory is high, and the current price is still mainly digested.

4. Inventory

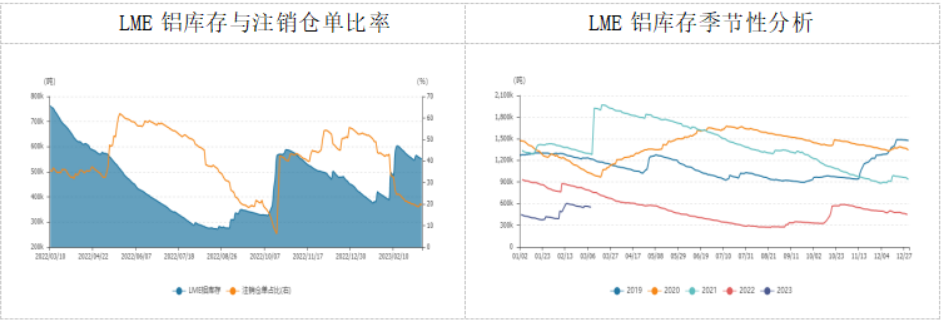

1. As of March 9, 2023, the LME aluminum inventory was 551,175 tons, an increase of 4,350 tons from the previous week, and the canceled warehouse receipts accounted for 19.65%.

2. As of March 9, 2023, the total social inventory of electrolytic aluminum was 1.193 million tons, a decrease of 11,000 tons from the previous week.

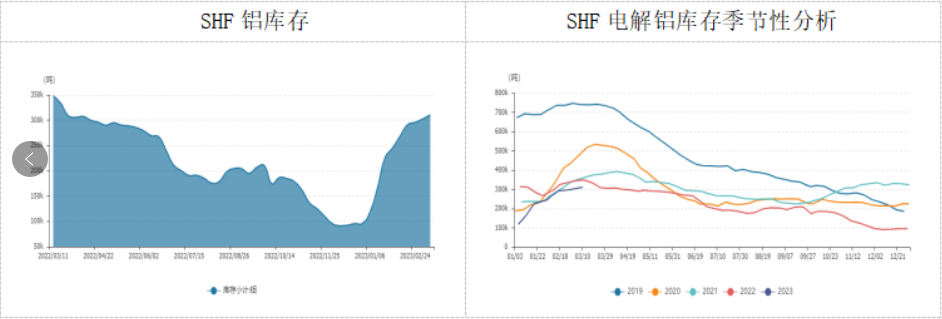

3. As of March 10, 2023, the electrolytic aluminum inventory of the Shanghai Futures Exchange was 310,888 tons, an increase of 8,289 tons from the previous week.

05

summary

On the supply side: Yunnan's production reduction has been implemented. Although Guangxi, Sichuan and Guizhou have resumed production to make up for part of the reduction, the operating production capacity has still dropped by nearly 700,000 tons, and due to the restart of production capacity, there will be no production supply and demand for the time being, and the actual production will drop. There is still a certain amount of imports, but it cannot make up for the reduction in production.

Consumer side: The performance of the terminal market is still dominated by seasonal mild recovery. The improvement in the sales of commercial housing in the real estate market is temporarily difficult to transmit to the completion end, so it has not yet been reflected in the consumption of aluminum profiles. Since the beginning of the year, the auto market has also cooled down significantly, subsidies have declined, and there are no policies to continue to affect the willingness to purchase, and it has not yet shaken off the fatigue. Exports continued to decline.

On the cost side: the change is small, the price of raw materials has not changed much, and the fluctuation of thermal coal price will not have direct feedback on the cost of electricity for the time being. Electrolytic aluminum maintains a good profit level.

Taken together: the short-term market will continue the pattern of slow improvement in supply and demand fundamentals. The output has declined in stages due to the reduction in production in Yunnan, and the supply side has declined. The margins on the consumer side continue to improve, but the overall demand is weak, the rhythm of the explicit inventory is relatively slow, and the explicit inventory is still at a high level. The recent macro sentiment has fluctuated greatly, especially the strengthening of the US dollar has put greater pressure on the external market. The market is still expecting consumption in the peak season, and aluminum prices may rebound as the inventory is eliminated. It is not recommended to chase the short in operation, and pay attention to the short-selling opportunities after the rebound.